Tax Deposit Example

- 19 Sep 2024

- 2 Minutes to read

- Print

Tax Deposit Example

- Updated on 19 Sep 2024

- 2 Minutes to read

- Print

Article summary

Did you find this summary helpful?

Thank you for your feedback!

This article shows how to record your payroll tax deposit payment with information from the tax deposit report.

Overview

Your payroll tax deposit includes both employee and employer amounts. Withholdings are liabilities you are paying on behalf of the employee, while Expenses are taxes the employer is responsible for paying. Some examples include Federal or State Income tax, Social Security and Medicare, Federal Unemployment (FUTA), State Unemployment (SUTA) and perhaps local taxes. Ask your accountant for details.

Tax Deposit Report

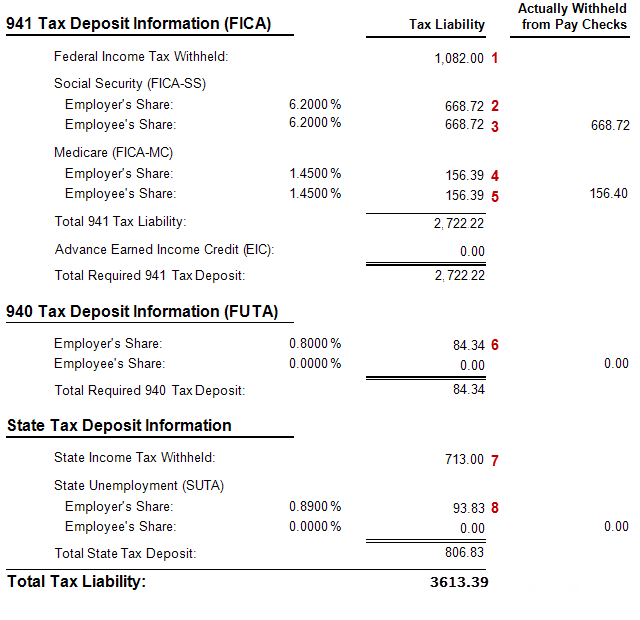

Print the tax deposit report to see the amount owed for a given period (see image below).

- Go to Reports > Standard Reports > Payroll > Tax Liability Summary > Tax Deposit Information.

- Enter a Date Range that includes the dates checks were posted, not the dates of the pay period.

The tax deposit report includes:

Amounts withheld from employees (the employee share) plus the employer share of Social Security, Medicare, FUTA and SUTA.

The tax deposit report does NOT include :

General Withholdings you have set up for each employee (like California SDI, Indiana County Tax, or other local taxes). If you are required to include such items on your tax deposit you’ll need to run another report for that information, such as the Payroll > Company Summary > Total Withholding Summary. Also, there may be other taxes paid only by the employer that are not tracked in Procare. Be sure to include any of these additional items in your actual tax deposit check.

Reading the report

Earnings: These are the amounts subject to taxation and used to compute taxes for the period. Taxable wages may be lower than gross earnings, if you have Pre-Taxed Withholdings such as certain retirement plans. For example, in the image below Total Federal Wages (taxable) are lower than Total Gross Earnings.

Actual Amounts Withheld versus Report Totals: You may notice slight differences between the Actually Withheld from Pay Checks column and the calculated amount. This is due to rounding differences when adding individual amounts withheld together, versus calculating based on the taxable earnings of everyone at once. For a single pay period the difference should be no more than a few cents and may be ignored.

941, 940 and State Amounts: These sections added together make up the grand total at the bottom. Notice the percentages for the employer’s share may differ from the employee’s share for FICA-SS, FICA-MC, FUTA and SUTA taxes along with the resulting liability or expense amount. Compare these red-numbered amounts to the example tax deposit check below.

Tax Deposit Vendor

It is recommended that you create a separate Vendor specifically for your tax deposit payment. This allows you to set the Standard Account Numbers to import, so all you need to change is the actual amounts being paid. For easy comparison, the order of the amounts in our example check match the order of the amounts withheld on the report.

Tax Deposit Check Example

The amounts for paying employee liabilities are entered as negative numbers because you are reducing the amount of the liability; the employer expenses are entered as positive numbers because you are increasing your expenses. See Debits and Credits for more detail.

Note: For clarity, we’ve modified the GL Account Name (in the Chart of Accounts) to indicate that expenses are the responsibility of the Employer, while liabilities where withheld from the Employee. You may wish to do the same.

Here is the example for the State portion of the tax deposit:

Was this article helpful?